In today’s economy, the rising cost of living has made it harder than ever to stay financially secure. A single unexpected expense — a car repair, a medical bill, or a job interruption — can quickly throw even the most careful budget off balance. For many households, these surprise costs lead to debt, stress, and a feeling of being stuck in a financial cycle that’s hard to escape.

The truth is, most people want to save, but when your income barely covers the basics — rent, groceries, utilities, and transportation — setting money aside feels almost impossible. The challenge isn’t a lack of discipline; it’s finding a realistic way to save when every dollar already has a purpose.

That’s where this guide comes in. You’ll discover practical, achievable strategies to start building your emergency fund — even if your budget is tight. From small daily habits to smart money tools, we’ll walk through simple steps you can take right now to create a financial safety net that brings peace of mind and long-term stability.

Because true financial wellness isn’t about how much you earn — it’s about how well you prepare for life’s unexpected moments.

Table of Contents

What Is an Emergency Fund and Why You Need One

What Is an Emergency Fund?

An emergency fund is a dedicated savings account set aside specifically for unexpected expenses or financial emergencies. It acts as a personal safety net, helping you handle sudden costs without derailing your budget or going into debt. Think of it as your financial “backup plan” — money you don’t touch unless life throws you an unavoidable curveball.

Why You Need an Emergency Fund

Life is unpredictable. Whether it’s a medical bill, car repair, job loss, or home maintenance issue, unexpected expenses can appear when you least expect them. Without a cushion in place, many people turn to credit cards, payday loans, or borrowing, which only leads to more financial stress and long-term debt.

An emergency fund gives you the freedom and confidence to handle these situations calmly. It ensures that one bad month doesn’t undo years of financial progress.

Key Benefits of an Emergency Fund

- Reduces Financial Stress: Knowing you have savings to fall back on offers emotional relief and stability.

- Prevents Debt Dependence: Keeps you from relying on credit cards, loans, or overdrafts during tough times.

- Provides Peace of Mind: Offers a sense of control and security, even when the unexpected happens.

In short, an emergency fund is your first line of defense against financial setbacks. It’s not about being overly cautious — it’s about being prepared. By setting aside even a small amount consistently, you build the foundation for long-term financial wellness and resilience.

How Much Should You Save in an Emergency Fund?

One of the most common questions people ask is, “How much emergency fund should I have?” The answer depends on your lifestyle, expenses, and financial comfort level — but there are some reliable guidelines to help you get started.

The General Rule of Thumb

Financial experts recommend saving three to six months’ worth of essential living expenses in your emergency fund. This amount provides a strong cushion to cover necessities like rent or mortgage, groceries, utilities, insurance, and transportation in case of income loss or major emergencies.

- Three months is often enough if you have a stable job, lower expenses, or a dual-income household.

- Six months or more is ideal if your income is variable, you’re self-employed, or you have dependents.

Having this amount ensures that you can maintain your basic standard of living without turning to debt when the unexpected happens.

If You’re on a Tight Budget — Start Small

Saving thousands of dollars might sound impossible right now, especially if you’re living paycheck to paycheck. But the key is to start where you are.

Your first milestone should be to save $500–$1,000 as a starter emergency fund. This smaller goal is achievable for most people and still provides protection against common small emergencies like car repairs or medical copays.

Even setting aside $10–$20 per week can get you there faster than you think. Consistency matters more than amount — every dollar counts.

How to Calculate Your Emergency Fund Goal

Use a simple formula or emergency fund goal calculator to estimate your target amount.

- List your essential monthly expenses:

- Rent or mortgage

- Utilities (electricity, water, internet)

- Groceries and basic supplies

- Transportation (fuel, public transit, car insurance)

- Minimum debt payments

- Add them up to find your total monthly need.

- Multiply by 3–6 to set your goal range.

Example:

If your monthly essentials cost $2,000, then:

- 3 months = $6,000

- 6 months = $12,000

Start with a smaller goal ($500–$1,000) and build gradually toward this target as your financial situation improves.

Bottom Line

Your emergency fund doesn’t have to be built overnight — it’s a journey. Begin small, stay consistent, and increase your goal as your income grows. The peace of mind that comes from being prepared is worth every dollar saved.

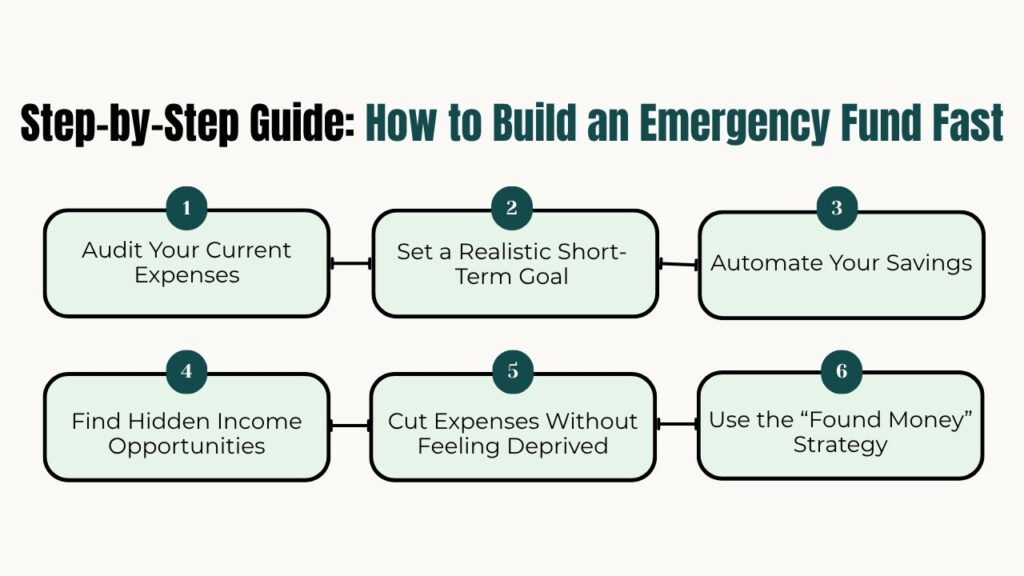

Step-by-Step Guide: How to Build an Emergency Fund Fast

Building an emergency fund doesn’t have to feel overwhelming — it’s about taking small, consistent actions that lead to big results. Follow this simple, step-by-step plan to start saving quickly, even if your budget feels tight.

Step 1: Audit Your Current Expenses

Before you can save, you need to understand where your money is going. Review your spending over the last few months to identify areas where you can cut back.

- Look for non-essential expenses such as unused subscriptions, takeout meals, impulse shopping, or streaming services you rarely use.

- Track your spending with a free budgeting app or spreadsheet to get a clear picture of your cash flow.

Once you identify unnecessary costs, you’ll see opportunities to redirect that money toward your emergency fund — without drastically changing your lifestyle.

Step 2: Set a Realistic Short-Term Goal

Start small and achievable. Instead of aiming for thousands of dollars right away, set a short-term target like saving your first $500 to $1,000.

Breaking it down helps:

- Save $10–$20 per week and you’ll reach your first goal in a few months.

- Celebrate small milestones along the way to stay motivated.

These micro-goals keep you engaged, making saving feel attainable rather than stressful.

Step 3: Automate Your Savings

Consistency is key — and automation makes it effortless. Set up an automatic transfer from your checking to a separate savings account each payday.

Even transferring a small, fixed amount each week builds momentum over time. By making savings automatic, you eliminate the temptation to skip or delay contributions.

You can also use digital banking tools or budgeting apps that round up your purchases or save small amounts automatically, helping your emergency fund grow in the background.

Step 4: Find Hidden Income Opportunities

If your budget is tight, look for creative ways to bring in extra income — even small amounts can make a big difference.

- Sell unused items online or through local marketplaces.

- Take on side gigs or short-term freelance work that fits your schedule.

- Monetize your skills or hobbies — tutoring, writing, or crafting can generate extra cash.

Every additional dollar you earn should go straight into your emergency fund. It’s one of the fastest ways to build your savings without touching your regular income.

Step 5: Cut Expenses Without Feeling Deprived

Saving money doesn’t have to mean giving up everything you enjoy. Focus on smart substitutions that help you spend less while maintaining your quality of life.

Practical ideas:

- Switch to more affordable mobile or internet plans.

- Cook at home instead of dining out — meal prepping saves time and money.

- Use cashback or reward apps when shopping.

- Buy in bulk or during sales for essentials.

These small changes can easily free up $50–$100 a month, accelerating your savings progress.

Step 6: Use the “Found Money” Strategy

Whenever you receive unexpected income — like a tax refund, work bonus, gift, or cashback reward — resist the urge to spend it. Instead, direct it immediately to your emergency fund.

You can also create a separate “buffer” account to keep this money untouched. Separating your emergency savings from daily spending ensures you won’t accidentally use it and keeps your progress visible.

Smart Tools and Accounts to Grow Your Emergency Fund

Once you’ve started saving, the next step is to make your money work smarter for you. The right tools and accounts can help you grow your emergency fund faster, with minimal effort. By using high-yield savings accounts, automation apps, and cashback programs, you can build momentum and reach your goals more efficiently.

Below are some of the best tools to save money fast and maximize your emergency fund growth.

1. High-Yield Savings Accounts

One of the most effective ways to grow your emergency fund is by keeping it in a high-yield savings account rather than a regular checking account. These accounts typically offer higher interest rates, allowing your savings to compound over time.

Why choose a high-yield account:

- Your money earns more interest while staying easily accessible.

- You’re less tempted to spend since it’s separate from your daily account.

- Most are online-based, offering low or no fees and flexible transfers.

When comparing options, look for:

- Competitive annual percentage yield (APY)

- No or minimal monthly fees

- Instant access without penalties

This setup ensures your emergency fund grows passively while staying available when you need it most.

2. Round-Up and Micro-Savings Apps

If saving feels difficult, round-up apps make it effortless. These tools automatically round up your purchases to the nearest dollar and save the spare change into your emergency fund.

For example, if you spend $7.50 on coffee, the app rounds it to $8 and saves the extra $0.50. It may seem small, but over time, these micro-savings add up significantly.

Benefits of round-up tools:

- Save money automatically without noticing it.

- Build consistent savings habits with zero effort.

- Perfect for those who struggle to save manually.

These apps are among the most practical tools to save money fast, especially for beginners who want an easy, hands-off approach to saving.

3. Cashback and Reward Programs

Cashback and reward platforms help you turn everyday spending into savings. Whether you’re shopping online or in stores, these programs return a percentage of your purchases as cash or rewards that can go directly into your emergency fund.

Ways to make the most of cashback programs:

- Use cashback credit or debit cards responsibly (pay balances in full).

- Sign up for apps or browser extensions that track eligible offers.

- Transfer earned rewards directly to your savings account instead of spending them.

Even small amounts — like 2%–5% cashback on essentials — can add up over time, giving your emergency fund a steady boost.

How to Stay Consistent When Motivation Fades

Starting your emergency fund is the easy part — staying consistent when motivation dips is where most people struggle. Saving money is as much about mindset as it is about math. When progress feels slow or life gets busy, the key is to turn saving into a habit, not a chore. Here’s how to stay on track and keep your financial momentum strong.

1. Build Saving Habits with Challenges

Gamify your savings journey by turning it into a fun, goal-oriented challenge.

- Try a 30-day no-spend challenge, where you avoid unnecessary purchases for a month and put the savings directly into your emergency fund.

- Do a weekly savings challenge, increasing the amount slightly each week — for example, $5 the first week, $10 the next, and so on.

- Create a spare change jar for physical cash, reinforcing daily saving behavior.

These challenges add excitement, structure, and a sense of progress, helping you stay focused even when your enthusiasm dips.

2. Reward Yourself for Milestones

Saving shouldn’t feel like punishment. Every milestone you hit — whether it’s your first $100, $500, or $1,000 — deserves recognition.

- Treat yourself to something small but meaningful, like a coffee date or a favorite snack.

- Record your achievements in a savings tracker or visual chart to see your progress grow.

By celebrating small wins, you reinforce positive behavior and keep the process enjoyable.

3. Reframe Saving as Self-Care and Freedom

Saving money isn’t about restriction — it’s about creating choices and security. Shift your mindset from “I can’t spend” to “I’m building freedom.”

When you view saving as self-care, it becomes an empowering act. Each dollar you save is an investment in your peace of mind, your future stability, and your ability to handle life on your own terms. This mental shift makes consistency feel natural rather than forced.

4. Introduce Accountability

Accountability helps transform intentions into action.

- Share your goal with a trusted friend, family member, or online community for support and encouragement.

- Use budgeting or savings apps that send reminders, progress alerts, and goal updates to keep you engaged.

- Consider a savings partner — someone who checks in weekly to celebrate progress or troubleshoot challenges.

Having others aware of your goals keeps you responsible and motivated, even when personal willpower wanes.

Common Mistakes to Avoid When Building an Emergency Fund

Creating an emergency fund is a smart financial move, but even well-intentioned savers can make mistakes that slow progress or reduce its effectiveness. Avoiding these common pitfalls ensures your fund truly serves its purpose — providing security and peace of mind when you need it most.

1. Using the Fund for Non-Emergencies

One of the most frequent mistakes is dipping into your emergency fund for non-urgent expenses, such as vacations, shopping sprees, or lifestyle upgrades.

- Remember, the fund is meant for unexpected costs like medical bills, car repairs, or temporary job loss.

- Using it for regular spending defeats its purpose and can leave you vulnerable when real emergencies arise.

Treat your emergency fund as a sacred safety net that you only tap in true financial emergencies.

2. Keeping Savings in Hard-to-Access Accounts

While it’s important to protect your money, placing your emergency fund in accounts that are difficult to access can backfire.

- Avoid investment accounts or long-term instruments that penalize early withdrawals.

- Your goal is liquidity, meaning you can access the money immediately when an emergency occurs.

The right balance is a safe, accessible savings account — ideally earning some interest while remaining ready for use.

3. Over-Saving While Ignoring Debt Priorities

Some people focus entirely on building an emergency fund while ignoring high-interest debt.

- If you’re carrying credit card debt or other high-interest loans, interest can accumulate faster than your savings grow.

- Strike a balance: save enough to cover small emergencies first, then allocate extra funds toward paying down debt.

This approach keeps you protected while reducing financial strain in the long run.

4. Ignoring Inflation and Interest Opportunities

Failing to account for inflation or low interest rates can erode the real value of your emergency fund over time.

- A fund sitting in a low-interest account may lose purchasing power in the long term.

- Consider high-yield savings accounts or micro-savings tools that let your money grow modestly while staying safe.

Optimizing your emergency fund for both safety and minimal growth ensures it maintains its value against rising costs.

Long-Term Strategy: Evolving Your Fund as Income Grows

Building your first emergency fund is just the beginning. Once you’ve established a starter fund, it’s time to think about long-term financial security. As your income grows and your expenses evolve, your emergency fund should grow too — creating a robust safety net that can weather larger financial challenges.

Expand Your Fund to Cover 6–12 Months of Expenses

After reaching your initial goal of $500–$1,000, gradually increase your emergency fund to cover six to twelve months of essential living costs. This larger fund provides a stronger safety net, protecting you from longer-term income disruptions like job loss or significant unexpected expenses.

- For example, if your monthly expenses are $2,500, aim for a fund between $15,000–$30,000 over time.

- Build it incrementally — even small increases each month add up and maintain your financial momentum.

Consider Tiered Savings for Financial Growth

A tiered savings approach allows you to manage risk, growth, and financial opportunities strategically:

- Level 1: Mini Emergency Fund ($500–$1,000)

- Covers minor emergencies and provides quick psychological relief.

- Perfect for getting started and building the habit of saving.

- Level 2: Full Emergency Fund

- Covers 3–6 months of essential expenses.

- Protects against larger, more serious financial setbacks.

- Level 3: Investment Transition Fund

- Once your emergency fund is secure, consider allocating excess savings toward low-risk investments or wealth-building opportunities.

- Helps your money work harder for you while maintaining an accessible safety net.

This tiered strategy balances security with growth, ensuring your savings serve multiple purposes over time.

Integrate Financial Wellness With Long-Term Goals

Your emergency fund should not exist in isolation. Integrate it with your broader financial wellness plan:

- Align savings with career changes, major life events, and personal goals.

- Combine emergency savings with retirement planning, debt reduction, and investment strategies.

- Regularly review and adjust your fund as your financial situation changes.

By evolving your fund as your income and expenses grow, you create a resilient financial foundation that supports both your short-term needs and long-term aspirations.

Conclusion

Financial security doesn’t happen overnight — it starts with small, consistent steps. Every dollar you save, no matter how little, builds momentum and strengthens your ability to handle life’s unexpected challenges.

Even saving a few dollars each week adds up over time, creating a sense of control and peace of mind that no quick fix can provide. The key is to start now and remain consistent, letting habit and discipline work in your favor.

Don’t wait for the perfect moment or extra income — start your first deposit today. Your future self will thank you for taking control, building resilience, and creating a financial safety net that ensures stability, freedom, and confidence.

Frequently Asked Questions

Q1. How can I save for an emergency fund if I live paycheck to paycheck?

Even on a tight budget, it’s possible to start an emergency fund. Begin with small, manageable amounts, like $10–$20 per week. Track expenses to identify areas to cut back, use automatic transfers to a separate account, and consider found money strategies like redirecting bonuses or cashback rewards to your fund.

Q2. Should I pay off debt or build an emergency fund first?

It depends on your situation. If you have high-interest debt, it’s often best to balance both: save a starter emergency fund of $500–$1,000 while making minimum debt payments. Once your mini fund is secure, prioritize paying off debt while continuing to grow your emergency savings.

Q3. Where should I keep my emergency fund — bank or cash?

Your emergency fund should be safe and easily accessible. A high-yield savings account is ideal because it earns interest while remaining liquid. Avoid keeping large amounts of cash at home, as it can be risky and doesn’t grow over time.

Q4. How long does it take to build an emergency fund?

The timeline depends on your savings rate and income. Starting with a small weekly or monthly contribution can help you reach a starter fund of $500–$1,000 in a few months. Expanding to cover 3–6 months of expenses may take a year or more, but consistency is key — even small contributions add up over time.

Q5. Can I use credit cards instead of an emergency fund?

Relying on credit cards is risky. Emergencies can lead to high-interest debt that grows faster than your ability to pay it off. An emergency fund provides liquidity, security, and peace of mind, which credit cards cannot guarantee. Use your emergency fund first and keep credit cards as a backup for extreme, unexpected situations.

Level up your life — explore our other personal development blogs for tips, strategies, and inspiration.